Medicare vs Medicaid Understanding Senior Care Coverage

Learn the key differences between Medicare and Medicaid and how they can help fund various senior living and care services.

Learn the key differences between Medicare and Medicaid and how they can help fund various senior living and care services.

Medicare vs Medicaid Understanding Senior Care Coverage

Navigating the world of senior care can feel like deciphering a complex code, especially when it comes to understanding how to pay for it. Two names you'll hear constantly are Medicare and Medicaid. While they sound similar, they are vastly different programs with distinct eligibility requirements and coverage benefits. For seniors and their families in the US and even those considering options in Southeast Asia, grasping these differences is crucial for making informed decisions about long-term care, assisted living, home care, and more.

Let's break down Medicare and Medicaid, exploring what each program offers, who qualifies, and how they can potentially help cover the significant costs associated with senior care. We'll also touch upon how these US-centric programs might influence decisions for those with international considerations.

Medicare Explained Your Federal Health Insurance Program for Seniors

Medicare is a federal health insurance program primarily for people aged 65 or older, certain younger people with disabilities, and people with End-Stage Renal Disease (ESRD). It's not based on income or assets; if you've paid Medicare taxes through your employment, you're generally eligible. Think of it as your primary health insurance once you reach a certain age or meet specific disability criteria.

Medicare Parts A B C D What Each Covers for Senior Health

Medicare is divided into several parts, each covering different services:

- Medicare Part A (Hospital Insurance): This covers inpatient hospital stays, care in a skilled nursing facility (SNF) for a limited time, hospice care, and some home health care. Most people don't pay a monthly premium for Part A if they or their spouse paid Medicare taxes for a certain number of years.

- Medicare Part B (Medical Insurance): This covers certain doctors' services, outpatient care, medical supplies, and preventive services. You typically pay a monthly premium for Part B, which can be deducted from your Social Security benefits.

- Medicare Part C (Medicare Advantage Plans): These are private insurance plans approved by Medicare that provide all your Part A and Part B benefits. Many Medicare Advantage Plans also offer extra benefits like vision, hearing, dental, and prescription drug coverage. They often have their own network of doctors and hospitals.

- Medicare Part D (Prescription Drug Coverage): This helps cover the cost of prescription drugs. It's offered through private insurance companies approved by Medicare. You can get Part D through a stand-alone plan or as part of a Medicare Advantage Plan.

Medicare and Long Term Care Limited Coverage for Senior Living

Here's a critical point: Medicare generally does NOT cover long-term care, such as extended stays in assisted living facilities, memory care, or ongoing custodial care at home. This is a common misconception that can lead to significant financial surprises for families.

However, Medicare Part A does cover short-term stays in a skilled nursing facility (SNF) if certain conditions are met. This is usually after a qualifying hospital stay (at least three consecutive days as an inpatient) and if you need skilled nursing care or therapy services. This coverage is limited, typically up to 100 days per benefit period, with a co-payment required after day 20.

Medicare Part B can cover some home health care services if you are homebound and need skilled nursing care or therapy on an intermittent basis. Again, this is for skilled care, not for ongoing personal care like bathing, dressing, or eating assistance (often referred to as 'custodial care').

So, while Medicare is excellent for acute medical needs, hospitalizations, and doctor visits, it's not designed to be the primary payer for long-term senior living or extensive in-home personal care.

Medicaid Explained Your State and Federal Assistance Program for Low Income Seniors

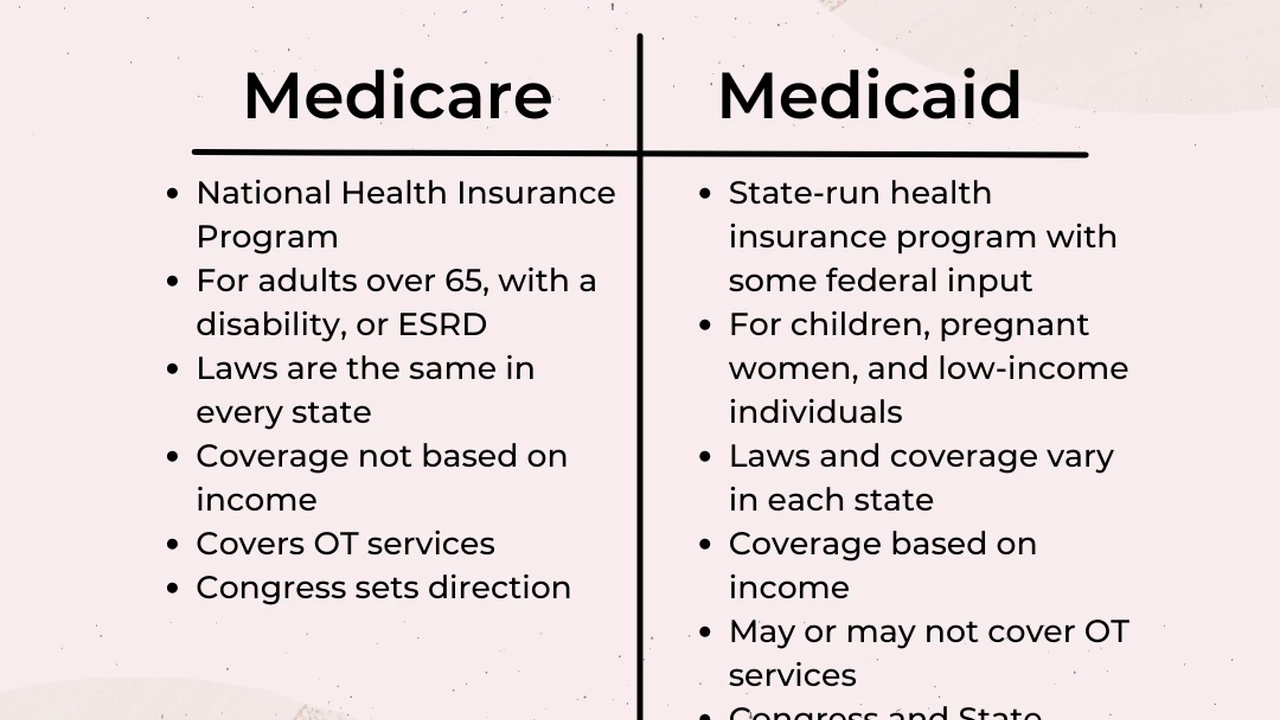

Medicaid is a joint federal and state program that helps cover healthcare costs for people with limited income and resources. Unlike Medicare, Medicaid is needs-based. Eligibility rules vary significantly from state to state, but generally, you must meet specific income and asset limits to qualify.

Medicaid Eligibility Income and Asset Limits for Senior Care

Qualifying for Medicaid for long-term care is often a complex process. States have strict limits on how much income and how many 'countable' assets an individual can have. For example, in many states, the asset limit for a single individual is around $2,000 (excluding certain exempt assets like a primary residence, one car, and some personal belongings). Income limits also apply, though some states have 'Medically Needy' programs where individuals with higher incomes can 'spend down' their income on medical expenses to qualify.

For married couples, there are specific rules to protect the spouse who is not applying for Medicaid (the 'community spouse') from becoming impoverished. These rules allow the community spouse to keep a certain amount of assets and income.

Medicaid and Long Term Care Comprehensive Coverage for Senior Living

This is where Medicaid shines for senior care. Medicaid IS the primary payer for long-term care services for eligible low-income individuals. This can include:

- Nursing Home Care: Medicaid covers the vast majority of nursing home costs for those who qualify.

- Assisted Living and Memory Care: Many states offer Medicaid waivers or programs that cover some or all of the costs for assisted living and memory care for eligible individuals. These waivers are designed to help people receive care in a less restrictive environment than a nursing home.

- Home and Community-Based Services (HCBS): Medicaid also funds a wide range of home care services, including personal care (bathing, dressing, eating), homemaker services, adult day care, and skilled nursing care at home, often through waivers. These programs aim to keep seniors in their homes and communities for as long as possible.

Because Medicaid is state-administered, the specific services covered and the eligibility criteria can differ significantly. It's crucial to check with your state's Medicaid agency or an elder law attorney to understand the rules in your specific location.

Key Differences Medicare vs Medicaid for Senior Care Funding

Let's summarize the core distinctions:

| Feature | Medicare | Medicaid |

|---|---|---|

| Primary Purpose | Health insurance for acute medical needs | Health coverage for low-income individuals, including long-term care |

| Eligibility | Age 65+, certain disabilities, ESRD (not income-based) | Income and asset-based (low-income and limited resources) |

| Funding | Federal program | Joint federal and state program |

| Long-Term Care Coverage | Very limited (short-term skilled nursing, some home health) | Extensive (nursing home, assisted living waivers, home care waivers) |

| Premiums | Part B and D usually have premiums | Generally no premiums for eligible individuals |

| Administration | Federal (CMS) | State-administered (rules vary by state) |

Navigating Both Medicare and Medicaid Dual Eligibility for Seniors

It's possible for seniors to be eligible for both Medicare and Medicaid. These individuals are often referred to as 'dual eligibles.' If you qualify for both, Medicare will be your primary insurance, covering your acute medical needs (doctors, hospitals). Medicaid then acts as a secondary payer, covering costs that Medicare doesn't, such as Medicare premiums, deductibles, co-insurance, and co-payments. Crucially, Medicaid will also cover the long-term care services that Medicare does not.

For dual eligibles, this combination can provide comprehensive coverage, significantly reducing out-of-pocket healthcare and long-term care expenses. There are special Medicare Advantage Plans called Dual Eligible Special Needs Plans (D-SNPs) designed specifically for individuals who have both Medicare and Medicaid, offering coordinated care and additional benefits.

Financial Planning Tools and Resources for Senior Care Costs

Since neither Medicare nor Medicaid might fully cover all your senior care needs, especially if you don't qualify for Medicaid, it's essential to explore other financial planning tools. Here are some key options and products to consider:

Long Term Care Insurance A Proactive Approach to Senior Care Funding

Long-term care insurance is designed specifically to cover the costs of services like assisted living, memory care, and in-home care. You purchase a policy, and if you later need long-term care, the policy pays out benefits. The earlier you buy it, the more affordable the premiums typically are. However, it can be expensive, and some people may not qualify due to pre-existing conditions.

- Product Examples: Companies like Genworth, Mutual of Omaha, and Northwestern Mutual are prominent providers.

- Use Case: Ideal for individuals who want to protect their assets and ensure they have choices for long-term care without relying solely on personal savings or qualifying for Medicaid.

- Comparison: Unlike Medicare, it directly covers custodial care. Unlike Medicaid, it's not income-dependent.

- Pricing: Highly variable based on age, health, benefit amount, and inflation protection. A 55-year-old couple might pay $3,000-$5,000 annually for a comprehensive policy.

Hybrid Life Insurance with Long Term Care Riders Combining Benefits

These policies combine life insurance with a long-term care benefit. If you need long-term care, you can access a portion of the death benefit while you're alive. If you don't use the long-term care benefit, your beneficiaries still receive a death benefit. This offers a 'use it or lose it' alternative to traditional LTC insurance.

- Product Examples: Many major insurers offer these, such as Nationwide, Lincoln Financial, and OneAmerica.

- Use Case: Good for those who want both life insurance coverage and a safety net for long-term care, ensuring that premiums aren't 'wasted' if care isn't needed.

- Comparison: Offers more flexibility than traditional LTC insurance and a guaranteed payout.

- Pricing: Can be more expensive than stand-alone life insurance but offers dual benefits. Premiums vary widely based on coverage.

Annuities for Senior Care Funding Converting Savings to Income

Certain types of annuities, particularly immediate annuities or deferred annuities with long-term care riders, can be used to generate a steady income stream to pay for care. A deferred annuity with an LTC rider allows you to access a multiple of your account value for long-term care expenses.

- Product Examples: Offered by many financial institutions, including New York Life, Fidelity, and Vanguard.

- Use Case: Suitable for individuals with a lump sum of savings they want to convert into a guaranteed income stream for future care needs.

- Comparison: Provides a predictable income, unlike relying on market fluctuations.

- Pricing: The cost is the principal amount you invest, and the payout depends on interest rates and the annuity's terms.

Reverse Mortgages Accessing Home Equity for Senior Care

A reverse mortgage allows homeowners aged 62 or older to convert a portion of their home equity into cash without having to sell the home or make monthly mortgage payments. The loan is repaid when the last borrower moves out, sells the home, or passes away.

- Product Examples: Lenders like American Advisors Group (AAG), One Reverse Mortgage, and Finance of America Reverse.

- Use Case: Excellent for seniors who own their home outright or have significant equity and need funds for in-home care or to supplement other senior living costs while remaining in their home.

- Comparison: Provides tax-free cash flow without selling the home, unlike a traditional home equity loan which requires monthly payments.

- Pricing: Involves closing costs, servicing fees, and interest that accrues over time.

Veterans Benefits Aid and Attendance for Wartime Veterans

The VA Aid and Attendance benefit is a little-known but significant resource for wartime veterans and their surviving spouses. It provides additional monetary assistance to those who require the aid of another person to perform daily activities, are bedridden, or reside in an assisted living facility or nursing home.

- Use Case: Crucial for eligible veterans or their spouses who need financial assistance for long-term care, including in-home care, assisted living, or nursing home care.

- Comparison: A non-service-connected pension benefit, meaning it's not tied to a service-related injury. It's needs-based but has different criteria than Medicaid.

- Pricing: This is a benefit, not a product you purchase. The maximum monthly benefit varies annually.

Considering Senior Care in Southeast Asia Financial Implications

For US citizens considering senior care options in Southeast Asia, understanding Medicare and Medicaid's limitations is even more critical. Generally, Medicare does NOT cover healthcare services received outside the US, with very few exceptions (e.g., if you're in Canada or Mexico and the nearest hospital is in the US). This means if you move to a country like Thailand, the Philippines, or Vietnam for retirement and care, Medicare will not pay for your medical expenses there.

Similarly, Medicaid is a US-based program and does not provide coverage for long-term care services received in other countries.

Therefore, if you're exploring senior living in Southeast Asia, you'll need to plan for private international health insurance, self-fund your care, or rely on local healthcare systems. Some US-based long-term care insurance policies might offer limited benefits for care received abroad, but this is rare and needs to be explicitly confirmed with the insurer. This makes robust personal financial planning, potentially utilizing the tools mentioned above, even more vital for international senior care.

Making Informed Decisions for Your Senior Care Journey

Understanding the roles of Medicare and Medicaid is the first step in building a solid financial plan for senior care. While Medicare handles your acute medical needs, it's not a long-term care solution. Medicaid can be a lifesaver for those with limited resources, covering extensive long-term care, but it requires meeting strict financial criteria.

For everyone else, or as a supplement to these programs, exploring options like long-term care insurance, hybrid policies, annuities, reverse mortgages, and veterans' benefits is essential. Don't wait until a crisis hits to start planning. Consult with a financial advisor specializing in elder care, an elder law attorney, or a benefits counselor to create a personalized strategy that ensures you or your loved ones receive the care needed without depleting life savings. The more you know, the better prepared you'll be to navigate the complex landscape of senior care funding, whether at home or abroad.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)