Transitioning Assets for Medicaid Eligibility A Guide

Get practical advice on asset protection strategies to help qualify for Medicaid while preserving family wealth.

Get practical advice on asset protection strategies to help qualify for Medicaid while preserving family wealth.

Transitioning Assets for Medicaid Eligibility A Comprehensive Guide to Protecting Family Wealth

Understanding Medicaid and Long-Term Care Costs

Navigating the complexities of long-term care can be overwhelming, especially when considering the financial implications. For many families in the United States, Medicaid becomes a crucial lifeline for covering the exorbitant costs of nursing home care, assisted living, and even some in-home care services. However, qualifying for Medicaid isn't as simple as just needing care. There are strict income and asset limits that can often seem daunting, leading many to believe they must spend down all their savings before receiving assistance. This guide aims to demystify the process of transitioning assets for Medicaid eligibility, offering practical advice and strategies to protect your family's hard-earned wealth while ensuring your loved one receives the care they need.

The average cost of a private room in a nursing home in the U.S. can easily exceed $10,000 per month, with assisted living facilities not far behind. These costs can quickly deplete a lifetime of savings, leaving families in a precarious financial position. Medicaid, a joint federal and state program, is designed to help low-income individuals and families pay for healthcare, including long-term care. However, to prevent individuals from simply transferring all their assets right before applying, Medicaid has specific rules regarding asset limits and look-back periods.

Medicaid Asset Limits and the Look-Back Period Explained

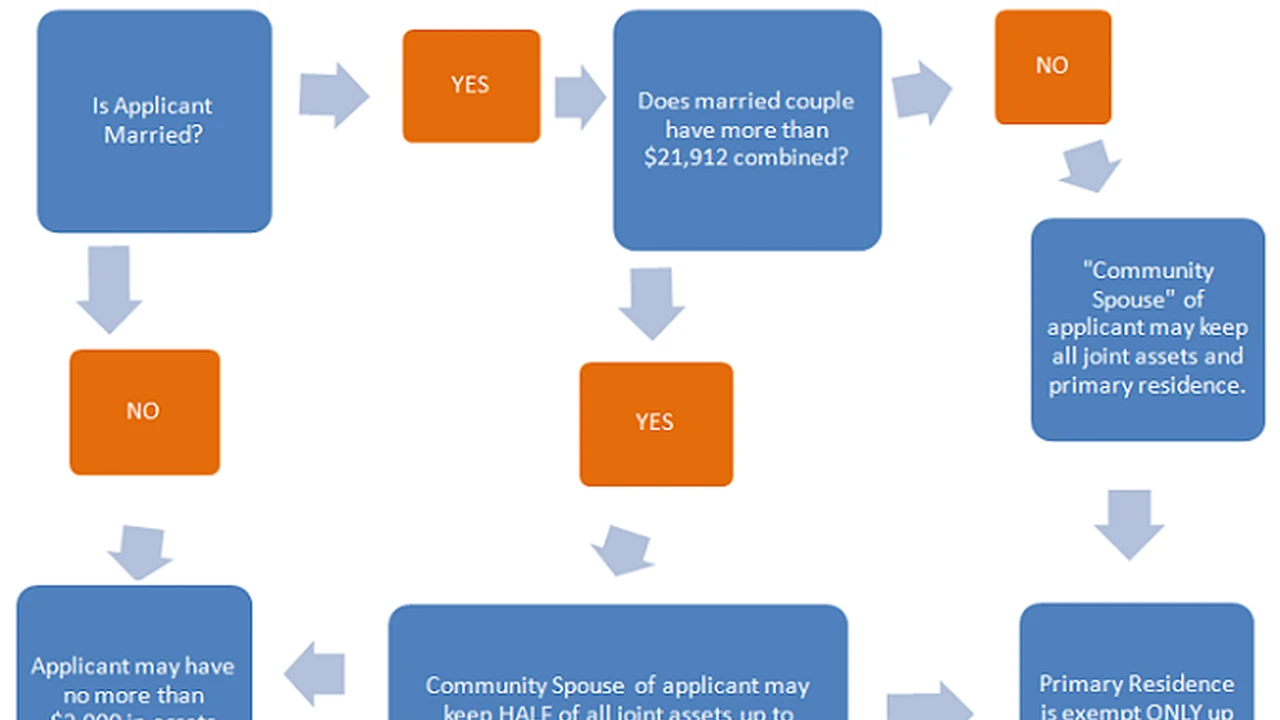

To qualify for Medicaid, applicants must meet certain income and asset thresholds. These thresholds vary by state and by the type of Medicaid program (e.g., institutional Medicaid for nursing home care). Generally, for a single individual, the asset limit is around $2,000, though some states allow slightly more. For married couples where one spouse needs long-term care and the other remains at home (the 'community spouse'), there are spousal impoverishment rules that allow the community spouse to retain a larger portion of assets, known as the Community Spouse Resource Allowance (CSRA). This amount also varies by state but typically ranges from approximately $27,480 to $137,400 in 2021, adjusted annually.

The most critical concept to understand when planning for Medicaid eligibility is the 'look-back period.' This is a period, typically 60 months (five years) in most states, during which Medicaid reviews all financial transactions made by the applicant. If any assets were transferred for less than fair market value during this period, Medicaid imposes a penalty period, during which the applicant is ineligible for benefits. The length of the penalty period is calculated by dividing the amount of the uncompensated transfer by the average monthly cost of nursing home care in that state. For example, if you gifted $100,000 and the average monthly cost of care is $10,000, you would be ineligible for 10 months.

Exempt Assets and Non-Countable Resources for Medicaid Planning

Not all assets are counted towards Medicaid's eligibility limits. Understanding what is considered an 'exempt asset' is crucial for effective planning. Common exempt assets include:

- Primary Residence: The applicant's home is usually exempt, provided its equity value is below a certain limit (e.g., $603,000 or $906,000 in 2021, depending on the state) and the applicant or their spouse intends to return home, or a dependent relative lives there.

- One Automobile: Typically, one vehicle of any value is exempt.

- Personal Belongings: Household goods, furniture, and personal effects are generally exempt.

- Life Insurance: Term life insurance policies are exempt. Whole life insurance policies are exempt if their face value is below a certain amount (e.g., $1,500).

- Burial Funds/Arrangements: Irrevocable burial trusts or pre-paid burial contracts are usually exempt up to a certain amount.

- Certain Retirement Accounts: In some states, certain retirement accounts (e.g., IRAs, 401ks) may be exempt if they are in 'payout status' (i.e., taking required minimum distributions).

It's important to note that rules regarding exempt assets can vary significantly by state, so consulting with an elder law attorney familiar with your state's specific regulations is highly recommended.

Effective Asset Protection Strategies for Medicaid Eligibility

While the look-back period and asset limits can seem restrictive, there are several legitimate strategies to protect assets and qualify for Medicaid. These strategies often require careful planning and should ideally be implemented well in advance of needing long-term care.

1. Irrevocable Trusts for Asset Protection

One of the most common and effective strategies is to transfer assets into an irrevocable trust. An irrevocable trust is a legal arrangement where you transfer ownership of your assets to a trustee, who then manages them for the benefit of designated beneficiaries (e.g., your children). Once assets are placed in an irrevocable trust, they are generally no longer considered yours for Medicaid eligibility purposes, provided the transfer occurred outside the 60-month look-back period. This means the assets are protected from being counted towards Medicaid's limits and are not subject to Medicaid estate recovery.

Product Recommendation: While not a 'product' in the traditional sense, establishing an irrevocable trust requires the expertise of an elder law attorney. Look for attorneys specializing in Medicaid planning and estate protection. For example, firms like Elder Law Associates PA or The Law Office of John Smith (hypothetical names, research local firms) offer comprehensive services in drafting and managing these trusts. The 'cost' here is the legal fees, which can range from $2,000 to $10,000+ depending on the complexity of your estate and the attorney's rates. The 'use case' is for individuals who want to protect significant assets (e.g., a family home, substantial savings) from being spent down for long-term care, ideally five or more years before care is needed.

2. Gifting and the Look-Back Period

Gifting assets to family members is another strategy, but it must be done carefully to avoid triggering the look-back period penalty. Any gifts made within the 60-month look-back period will result in a penalty. However, if gifts are made more than five years before applying for Medicaid, they will not be penalized. This strategy is often used for smaller amounts or when there's a long planning horizon.

Consideration: While seemingly straightforward, gifting can have tax implications for the recipient and the donor. It's crucial to understand the annual gift tax exclusion (e.g., $17,000 per recipient in 2023) and lifetime gift tax exemption. Consult with a financial advisor or elder law attorney before making significant gifts.

3. Purchasing Exempt Assets

As mentioned, certain assets are exempt from Medicaid's asset limits. You can strategically convert countable assets into exempt assets. For example, you could use excess cash to pay off a mortgage on your primary residence (if it's within the equity limit), purchase an irrevocable burial trust, or buy a new, more reliable vehicle. These actions reduce your countable assets without incurring a penalty, as you are not transferring assets for less than fair market value; you are simply changing their form.

Product Recommendation: For burial arrangements, consider companies like Dignity Memorial or local funeral homes that offer pre-paid, irrevocable burial plans. These plans allow you to lock in today's prices and ensure your final wishes are met without burdening your family financially. The 'cost' varies widely based on the services chosen, typically ranging from $5,000 to $20,000+. The 'use case' is for individuals who want to reduce countable assets while also planning for end-of-life expenses in a Medicaid-compliant way.

4. Spousal Refusal and Community Spouse Resource Allowance (CSRA)

For married couples, spousal impoverishment rules are designed to prevent the community spouse from becoming impoverished when the institutionalized spouse applies for Medicaid. The community spouse is allowed to keep a certain amount of assets (the CSRA) and a portion of the couple's income (the Minimum Monthly Maintenance Needs Allowance, MMMNA). In some states, a strategy known as 'spousal refusal' or 'spousal impoverishment' can be employed. This involves the community spouse refusing to contribute their assets towards the institutionalized spouse's care, which can allow the institutionalized spouse to qualify for Medicaid. However, the state may then pursue the community spouse for reimbursement, making this a complex strategy that requires legal guidance.

5. Medicaid Compliant Annuities

A Medicaid Compliant Annuity (MCA) is a specialized financial product that can be used to convert a countable asset (like a lump sum of cash) into an income stream for the community spouse. This strategy is particularly useful when one spouse is entering a nursing home and the couple has assets above the CSRA. The MCA must be irrevocable, non-assignable, actuarially sound (meaning the payout period does not exceed the annuitant's life expectancy), and name the state Medicaid agency as the primary beneficiary for any remaining funds up to the amount of Medicaid benefits paid. This allows the institutionalized spouse to qualify for Medicaid while providing income for the community spouse.

Product Recommendation: Several insurance companies offer Medicaid Compliant Annuities. Examples include Genworth Financial, New York Life, and various smaller, specialized annuity providers. You'd typically work with a financial advisor specializing in elder care planning or an elder law attorney to set this up. The 'cost' is the lump sum premium paid for the annuity, which can be tens or hundreds of thousands of dollars, plus any advisor fees. The 'use case' is for married couples where one spouse needs long-term care, and the couple has excess countable assets that need to be converted into an income stream for the community spouse to meet Medicaid eligibility requirements.

6. Promissory Notes and Loans

In some situations, a Medicaid applicant can loan money to a family member in exchange for a promissory note. If structured correctly, this can convert a countable asset (cash) into an exempt asset (a promissory note that is considered an asset but not counted towards the limit if it meets specific criteria). The loan must be for fair market value, have a reasonable interest rate, and be repaid within the applicant's life expectancy. This is a highly complex strategy and must be executed perfectly to avoid triggering a penalty.

Comparing Asset Protection Products and Strategies

Let's break down some of these strategies and 'products' in a comparative way:

| Strategy/Product | Primary Use Case | Pros | Cons | Typical Cost/Investment | Ideal Timing |

|---|---|---|---|---|---|

| Irrevocable Trust | Protecting significant assets (home, savings) from Medicaid estate recovery and eligibility limits. | Strong asset protection, avoids probate, maintains family control over assets (via trustee). | Assets are permanently out of your control, subject to 5-year look-back period, legal fees. | $2,000 - $10,000+ (legal fees) | 5+ years before needing long-term care. |

| Medicaid Compliant Annuity (MCA) | Converting excess countable assets into an income stream for a community spouse. | Allows institutionalized spouse to qualify for Medicaid, provides income for community spouse. | Irrevocable, state becomes beneficiary for remaining funds, complex rules. | Lump sum premium (e.g., $50,000 - $200,000+) | When one spouse needs immediate long-term care and assets exceed CSRA. |

| Irrevocable Burial Trust | Pre-paying for funeral expenses to reduce countable assets. | Reduces countable assets, ensures funeral wishes are met, protects funds from Medicaid. | Funds are locked in, limited flexibility once established. | $5,000 - $20,000+ (based on funeral choices) | Anytime, but especially useful when approaching Medicaid eligibility. |

| Gifting (outside look-back) | Transferring smaller assets to family members. | Simple, can reduce estate size. | Subject to 5-year look-back, potential gift tax implications, loss of control. | Amount gifted | 5+ years before needing long-term care. |

| Paying off Mortgage/Debt | Converting countable cash into an exempt asset (home equity). | Reduces countable assets, eliminates debt. | Only applicable if home equity is within limits, cash is no longer liquid. | Amount of debt paid | When approaching Medicaid eligibility, or anytime. |

The Importance of Professional Guidance in Medicaid Planning

Medicaid rules are incredibly complex and vary significantly from state to state. Attempting to navigate these rules without professional guidance can lead to costly mistakes, including lengthy penalty periods, loss of benefits, and even legal repercussions. An experienced elder law attorney can:

- Assess your specific financial situation and long-term care needs.

- Identify all countable and exempt assets.

- Develop a personalized Medicaid planning strategy tailored to your goals.

- Draft necessary legal documents, such as irrevocable trusts or promissory notes.

- Assist with the Medicaid application process and represent you in appeals if necessary.

- Ensure compliance with all state and federal Medicaid regulations.

Beyond legal counsel, a financial advisor specializing in elder care or long-term care planning can also be invaluable. They can help you understand the financial implications of various strategies, recommend appropriate financial products like Medicaid Compliant Annuities, and help manage your assets in a way that aligns with your overall financial goals.

Common Pitfalls to Avoid in Medicaid Asset Transitioning

While planning, be aware of these common mistakes:

- Waiting Too Long: The 60-month look-back period is a significant hurdle. Starting your planning early is the single most important factor for successful asset protection.

- Uncompensated Transfers: Gifting assets without proper planning or within the look-back period will almost certainly result in a penalty.

- Ignoring State-Specific Rules: Medicaid rules are not uniform across the U.S. What works in Florida might not work in California.

- Not Updating Plans: Life circumstances change, and so do Medicaid rules. Regularly review and update your plan with your attorney.

- Failing to Disclose Information: Always be transparent with Medicaid about all financial transactions. Hiding assets can lead to severe penalties, including criminal charges.

- Relying on Bad Advice: Be wary of advice from non-professionals or those promising quick fixes. Always consult with a qualified elder law attorney.

Case Studies and Real-World Scenarios for Asset Protection

Let's look at a couple of hypothetical scenarios to illustrate how these strategies might play out:

Scenario 1: The Proactive Planner (5+ Years Out)

Mary, a single woman, is 70 years old and in good health, but she's concerned about potential future long-term care costs. She owns a home worth $400,000 and has $250,000 in savings. Her state's Medicaid asset limit for a single person is $2,000, and the home equity limit is $603,000.

Strategy: Mary consults an elder law attorney. Five years before she anticipates needing care, she establishes an irrevocable trust and transfers her home and $200,000 of her savings into it. She keeps $50,000 in a separate account for immediate needs. After the 5-year look-back period passes, these assets are no longer countable for Medicaid. If Mary needs nursing home care at age 76, she can apply for Medicaid, and her home and the bulk of her savings will be protected for her beneficiaries.

Scenario 2: The Crisis Planner (Immediate Need)

John and Jane are a married couple. John, 80, has had a sudden stroke and needs immediate nursing home care. They have a home worth $350,000, $150,000 in a joint savings account, and John's monthly income is $2,500, while Jane's is $1,000. Their state's CSRA is $137,400, and the asset limit for the institutionalized spouse is $2,000.

Strategy: Their combined countable assets ($150,000) exceed the CSRA. They consult an elder law attorney. The attorney advises them to use $12,600 of their excess savings to purchase an irrevocable burial trust for John. The remaining $137,400 is protected under the CSRA for Jane. John's income will go towards his care, but Jane will receive a portion of it as her MMMNA. This allows John to qualify for Medicaid without Jane having to spend down all their joint savings.

Navigating Medicaid Estate Recovery and Protecting Inheritances

Even after an individual qualifies for Medicaid and receives benefits, there's another crucial aspect to consider: Medicaid Estate Recovery. Federal law requires states to recover the costs of Medicaid long-term care services from the estates of deceased Medicaid recipients. This means that after a Medicaid recipient passes away, the state can place a lien on their home or other assets to recoup the money spent on their care. This can be a significant concern for families hoping to pass on an inheritance.

However, proper asset protection planning, particularly through the use of irrevocable trusts, can shield assets from Medicaid estate recovery. When assets are transferred into an irrevocable trust and the look-back period has passed, those assets are no longer considered part of the Medicaid recipient's estate upon their death. Therefore, they are generally protected from estate recovery claims. This is a primary reason why many families choose to engage in proactive Medicaid planning.

There are also certain exceptions and limitations to estate recovery, such as when there is a surviving spouse, a child under 21, or a disabled child of any age. Additionally, states may have hardship waivers. An elder law attorney can help you understand these nuances and implement strategies to minimize the impact of estate recovery on your family's inheritance.

The Future of Medicaid Planning and Long-Term Care

The landscape of long-term care and Medicaid eligibility is constantly evolving. Legislative changes, economic shifts, and demographic trends all play a role in shaping future policies. As the population ages, the demand for long-term care services will continue to grow, putting pressure on existing funding mechanisms. This makes proactive and informed planning even more critical.

Staying informed about potential changes in Medicaid law, consulting with professionals regularly, and adapting your plan as needed are essential steps in ensuring your long-term care needs are met while protecting your financial legacy. The goal isn't to 'hide' assets, but to legally and ethically arrange your finances to comply with Medicaid rules, allowing you to access vital care without completely depleting your family's resources. It's about smart planning for a secure future.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)